2022 set the tone for a turning point in China’s economy. After several COVID-19 outbreaks throughout the year, which led to a widespread economic slowdown, Beijing has abandoned the most stringent aspects of its Zero-Covid policy to facilitate the resumption of industrial activity and speed up production.

In response to Beijing’s shift to “living with COVID”, analysts have raised their forecasts for China’s real GDP growth to 5.2 percent in 2023 (from 4.7 percent) and 4.8 percent in 2024 (from 4.5 percent). Analysts at J.P. Morgan increased their estimates of the country’s annual growth rate to 4.3 percent from 4 percent.

That said, in coming months, China’s economy will still face several internal and external headwinds, such as weak domestic consumption, declining business confidence, and disruptions caused by the surge of COVID-19 infections. This has prompted calls for strong and focused policies to help restore private sector business activity in 2023.

Unsurprisingly, top leaders and policymakers were committed to accelerating policy measures to bolster the faltering economy at the 2022 closed-door Central Economic Work Conference (CEWC). Indeed, as set out in the CEWC, China will double down on economic growth in 2023, with anticipated measures to boost domestic demand, attract and utilize foreign capital, stabilize the housing market, and restructure the technology industry.

Against this background, analysts have predicted that China’s economy will be able to see an above-trend sustained rebound starting from the second quarter of 2023, following the country’s reopening.

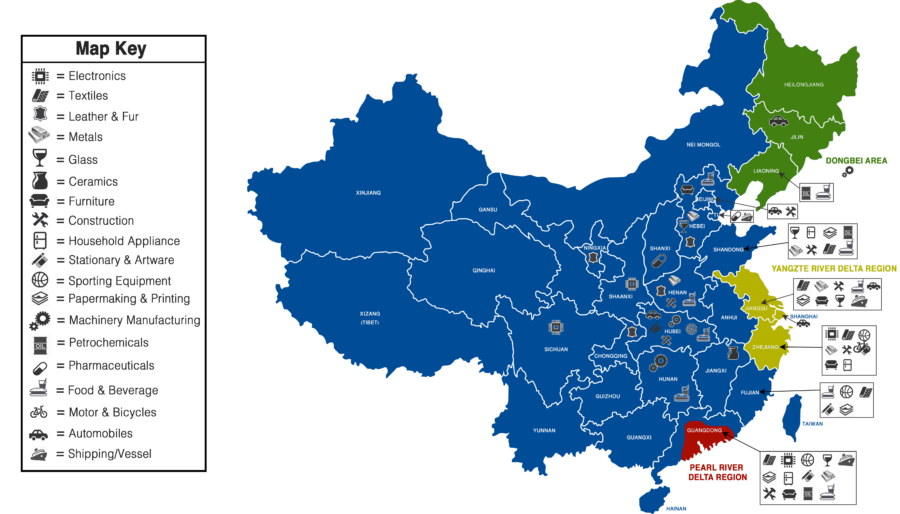

In this article, we look into the Chinese industries that are likely to experience strong growth in 2023.

The tourism and entertainment industry has a positive outlook for 2023, thanks to a more relaxed COVID policy and further opening.

The COVID-19 pandemic has had a catastrophic effect on the tourism sector, and due to stringent quarantine rules for visitors entering China, in the past two years, the majority of Chinese customers have been prevented from traveling abroad. However, the sheer scale of the local customer base, which has been eagerly rediscovering the country and its beautiful landscape, has allowed China’s tourism sector to rebound dramatically.

Camping and outdoor activities have become extremely popular since the start of the pandemic, and will likely continue to be so. Indeed, the growing popularity of camping is proof of the Chinese tourism sector’s adaptability and durability, as well as the kinds of novel opportunities that may materialize even in the face of severe constraints, proving that the industry will continue to grow.

Moreover, demand for industry services is expected to rebound over the next five years. The hotel sector’s structure will continue to change, with a larger portion of industry income coming from three- and four-star hotels. Foreign businesses now control the high-end industry, but they have recently been expanding into the lower star-rated segment to attract a wider range of clients and solidify their market positions.

Looking at China’s catering sector, revenue from cafes, bars, and other drinking establishments is anticipated to rise to RMB 6.03 trillion (US$894.36 billion) by the end of 2023. Coffee shops, for example, are expected to grow by 5 percent over the next five years, adding a total of 120,000 stores across the country. Revenue generated by the bar industry is projected to reach US$29.4 billion by 2025, with an impressive CAGR of 18.8 percent. As China continues to open up, people are likely to spend more on these types of activities.

Automotive is a key industry for developing countries like China, as it hosts an array of second and third-tier manufacturers, all supporting the major global manufacturers.

The new energy vehicles (NEVs) and automobile manufacturing industries in China have seen rapid growth. This has mainly been driven by the central government’s supportive policies and subsidies, growing environmental concerns, increased number of charging stations, and decreased operating costs for NEVs. Between 2017 and 2022, the industry revenue increased by 48.1 percent annually, and the industrial output grew from 794,000 units to over 5.6 million units in the same period. The China Association of Automobile Manufacturers (CAAM) predicted that China’s NEV sales in 2023 would grow by 35 percent year-on-year to 9 million units.

The NEV industry segment is expanding at an unprecedented rate, as part of Beijing’s conscious efforts to lower its carbon footprint while exploring the multi-billion-dollar market segment. In 2020, the Chinese government first introduced new measures to support the NEV industry – electric vehicles, plug-in hybrid vehicles, and fuel cell vehicles – which had been negatively impacted by the COVID-19 pandemic. It then announced the extension of tax exemption for NEV customers throughout 2023 as part of its plan to achieve 20 percent NEV deployment by 2025. Meanwhile, the question for 2023 remains whether the market can shift toward more stable growth with less government intervention on the production side of the industry or whether Beijing will once again step in to support the sector expansion.

Meanwhile, competition in the sector for 2023 is also expected to grow, as dozens of new models are expected to debut in the new year from tech giants, such as Baidu, and smart NEV manufacturers, such as Xpeng and Nio.

One important consideration is that China is the world’s leading lithium-ion battery manufacturer, the batteries that are used in most electric cars. While the bulk of the world’s lithium resources is held by other countries, China has acquired the highest number of lithium mines abroad, further indicating that its future will be electric.

China’s e-commerce market – the largest in the world – grew by 10.4 percent in 2022 as customers rapidly transitioned from traditional retail to online shopping. The industry is anticipated to grow at a compound annual growth rate (CAGR) of 11.6 percent between 2021 and 2025, eventually reaching RMB 21.4 trillion (US$3.3 trillion). The percentage of e-commerce platform users is expected to reach 83.9 percent over the same period, with an estimated 1,230.4 million active users.

By the end of 2022, China’s e-commerce livestreaming market is projected to generate RMB 1.2 trillion (US$180 billion) in total revenue, with a total of 660 million viewers. This figure is anticipated to increase even further in 2023 to reach RMB 4.9 trillion (US$720 billion). Livestreaming functions as a means for boosting sales and brand awareness and has rapidly grown to become an essential tool for businesses that embark on online selling.

Foreign investors who are eying China’s enormous domestic market are encouraged to fully leverage its huge online shopping channels in 2023.

Goldman Sachs anticipates that China’s software sector will achieve revenue growth of 28 percent year-on-year in 2023, compared to 14 percent in 2022. In terms of the automotive software segment, top picks include Thundersoft, DeSe, and ArcSoft Corp, while in the cyber security software segment, expectations are high for Beijing VenusTech. The smartphone segment, however, is expected to remain flat throughout 2023, while high-tech electronics look very promising.

Generally speaking, the industry is projected to grow by 14.67 percent between 2022 and 2027, reaching a volume of US$50.05 billion. In particular, the application development software segment will grow by 16.17 percent over the same period.

Meanwhile, Beijing is paving the way for its high-tech sectors to thrive. In 2022, the government released the country’s first national-level policy document for the development of technologies related to the metaverse (the “Action Plan”), including virtual reality (VR), augmented reality (AR), and mixed reality (MR). VR is also listed among the “key industries” for the digital economy in the 14th Five-Year Plan (FYP), China’s overarching economic and industrial development plan for the period from 2021 to 2025. The Action Plan is a clear signal that the Chinese government is banking on VR technology and the metaverse to become the next big thing in the digital space.

Revenue in the AR and VR sectors is expected to reach US$5.43 billion by the end of 2022, and it is estimated to grow by 14.64 percent annually in the years leading up to 2027, resulting in a total market volume of US$10.75 billion.

China’s health industry is expanding at an unprecedented rate. The sector has grown to be the second biggest in the world due to a number of factors, including a longer life expectancy, an aging population, and higher aspirations for quality of life.

In addition, since the Healthy China 2030 project was launched in 2016, there has been considerable investment in local healthcare infrastructure, market reforms, and assistance for innovation. The delivery of healthcare services is becoming increasingly effective thanks to this project. The COVID-19 pandemic and related travel restrictions have also sped up the development and uptake of online medical and pharmaceutical services in China, further contributing to the industry’s modernization.

Between 2023 and 2024, the industry is anticipated to expand at a CAGR of 39 percent.

Several research firms estimate considerable growth in the biotech and pharmaceutical sector, which will be worth over US$90 million in 2023. This is especially true given the increasing investment in cutting-edge therapies. Nowadays, biotech medications are preferred over conventional ones due to their reduced adverse effects.

The Chinese government’s R&D investment in biotech exceeded US$291 billion in 2019, and by 2020, Chinese companies accounted for almost a third of all biotech IPOs worldwide. As a result, biotech has also emerged as a crucial field for Chinese innovation and is supported by several preferential policies, such as interest-free loans and land incentives.

With China officially reopening its borders and abolishing its “zero-COVID” policies, sectors and fields that have been seriously affected by COVID-19 prevention and control will also become those with a larger margin for rebound and expansion in 2023. These include (but are not limited to) services, travel, and entertainment. In addition, promising industries which align with the government’s plan for development and innovation are likely to continue to benefit from Beijing’s policy support and incentives.

By Giulia Interesse on January 12 2023 for the China Briefing.