Almost a decade has passed since President Xi Jinping announced the launch of the Belt and Road Initiative (BRI), originally titled ‘One Belt One Road’. The BRI has since expanded into one of China’s most important tools for the build-up of soft power and the implementation of its overseas activities (Dadabaev, 2018). Simultaneously, however, the initiative has attracted controversy in the international media, particularly after COVID-19 led to widespread disruption of global economic activity1. The downturn caused debt distress in many developing countries, many of which received massive Chinese investment prior to 2020. This raises the question as to how the sentiment towards the BRI has evolved across the globe.

On the positive side, the BRI has supplemented existing official development assistance from institutions such as the World Bank and the Asian Development Bank. With massive financing, China has provided large-scale infrastructure investment to Belt and Road countries. Prior to the COVID-19 pandemic, recipient countries, especially those lacking the financial means to satisfy their need for investment, were generally optimistic about the initiative.

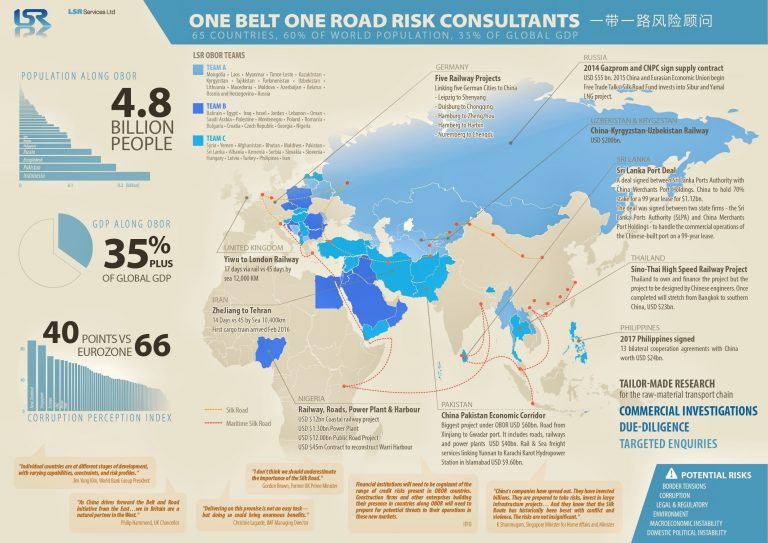

By 2022, the BRI had officially expanded to 149 member states. In 2018 alone, the number of countries with Memorandums of Understanding with China almost doubled. The literature has confirmed the potential benefits China could bring to Belt and Road countries, especially through trade and investment channels. García-Herrero and Xu (2017) estimated Europe’s expected trade gains as 6 percent above the non-BRI benchmark case, and 3 percent above trade gains in Asia. The rest of the world would suffer a reduction in trade of 0.004 percent.

Case studies for specific countries have equally portrayed a potential for positive impact. A study by the World Bank found that trade and investment flows under the BRI could increase Azerbaijan’s GDP by 21 percent in the long run, depending on the implementation of complementary policies such as the harmonisation of transportation tariffs and legal conditions across the region. Additionally, Li (2018) found that the two international transport corridors (Primorye-1 and Primorye-2) under the BRI linking East Siberia with the Asia-Pacific region provide new opportunities for Russia as well.

Critics have pointed out that projects initiated under the BRI umbrella lack the appropriate regulatory framework and market coordination. Without relying on market mechanisms, countries run the risk of engaging in too many projects simultaneously, which is likely to be unprofitable in the long run. Given that most of China’s financial support is to be repaid, debt sustainability in the host countries has become a concern. For instance, Sheng (2018) studied China’s investment transactions in Uzbekistan and Bangladesh and found that BRI-related investment stands at a value of over 20 percent of their gross domestic product (GDP). Watchers also doubt whether China has full economic strength to sustain ‘non-profitable’ overseas projects without coordinating with enough commercial interests. Beyond legal and economic aspects, international backlash can come from diplomatic considerations. For instance, India is aware of being isolated if the BRI gains strong support.

Eventually, circumstances have radically changed with the onset of the COVID-19 pandemic. Lockdowns all around the world inflicted a heavy toll on the global economy and stimulus for an economic revival has consumed large amounts of financial capital. Previous concerns about debt sustainability materialised. Indeed, China’s lending had already declined before the pandemic and debt renegotiations became more common. However, the pandemic has worsened the financial situation in many developing countries. Sovereign debt restructurings with China increased to a total number of 15 in 2020, and 18 in 2021, up from five in 2019. In some cases, negotiations were preceded by debt default. For instance, Sri Lanka – a major recipient of Chinese investment – defaulted in April 2022. In September 2022 it started negotiations with its largest bilateral creditors, namely China, India, and Japan.

Given the ambiguous views of the Belt and Road Initiative, it is important to offer a comprehensive and quantitative assessment of the image of the BRI across the globe, both in BRI member countries and non-member countries. This paper conducts an analysis of international media sentiment towards the BRI based on the Global Database of Events, Language, and Tone (GDELT), a big data platform covering international and local media. A growing literature using big data to analyse economic outcomes already exists. For example, Narita and Yin (2018) constructed the Search Volume index (SVI) to measure the frequency of online searches on key economic topics and use them as alternative indicators for economic assessment. Hlatshwayo et al (2018) used the database Factiva to calculate the news coverage of corruption activities across countries. Factiva has also been used to study the evolving sentiment towards the BRI inside and outside China. However, the authors use Factiva, which does not allow a representative large-N sample to be obtained. For most countries only a single article is available. GDELT offers the possibility of a more comprehensive analysis. Besides, GDELT’s contribution as a big data source to examine the connection between countries has also proven to be powerful in other contexts

Our results are as follows. First, the initiative is generally positively received in the world. In fact, all regions, except South Asia and North America, hold a positive average image of the BRI. However, the differences are sometimes only visible at the country level with all regions – except Central Asia – having at least one country with strongly negative sentiment. Second, perhaps not surprisingly, BRI countries have a slightly more positive view towards the BRI than do non-BRI countries. Third, we find that the image of the BRI has deteriorated faster than the image of China as a whole, but not with the same magnitude across regions. Sentiment is still strongly positive in Central Asia and sub-Saharan Africa but has decreased significantly in North America and Europe.

Before conducting the sentiment analysis, we document news coverage on the Belt and Road Initiative in general using Factiva. Although the initiative itself was labelled as China’s flagship project in its foreign engagement, the world’s attention towards the concept was quite scarce in the first two years after its establishment. In 2013, the year when the initiative was first launched, the percentage of BRI related news only accounted for 0.04 percent of all the China-related articles. Since then the number of BRI news has grown rapidly, first increasing to 0.12 percent in 2015, and then jumping to 0.56 percent within one year from 2016 to 2017. Since the pandemic the percentage of BRI-related news has declined again to an average of approximately 0.27 percent. In sum, this means that the BRI is still covered in the news although attention has shifted to other topics in China-related coverage during the pandemic. It also provides confidence that our period limit imposed by GDELT is not a serious issue for the validity of the analysis.

Having confirmed the importance of the BRI in coverage about China, we calculate the average sentiment for each individual country as laid out in Section 2. Considering all countries in our sample, the mean (0.67) and median sentiments (0.49) for the Belt and Road Initiative are above zero, indicating that the Initiative is on average rather positively received. Among all the countries, the highest sentiment rating is 4.62 in Monaco, and the lowest sentiment is -1.86 for Kosovo. There is great variance across geographies in overall sentiment. The regions that are most positive towards the BRI are visibly sub-Saharan Africa and Centra Asia. We further quantify this in Section 3.4. In contrast, the US, Canada, the United Kingdom and Australia are uniformly critical of the BRI. Next, we turn to a deeper analysis of our data.

For our statistical analysis, we exclude countries for which fewer than ten articles are available over the close to six-year period. We do this in order to not have our results driven by outliers whose media sentiment is shaped by specific events. This leaves us with sentiment data on 148 countries across all continents. In Figure 3, we further show the decomposition of countries into ‘Early Joiners’, ‘Late Joiners’, and ‘Non BRI Countries’. Each dot on the line represents an individual country on the sentiment scale, while the red points are the average of each group, as calculated by the mean. Unsurprisingly, the Belt and Road Initiative is received significantly more negative in countries that – as of early 2023 – have not signed an MoU yet. ‘Non BRI Countries’ hold an average sentiment of -0.13. In contrast, ‘Early Joiners’ and ‘Late Joiners’ hold an average sentiment of 0.65 and 0.86, respectively. This result still holds as we exclude the extreme observations, namely Turkmenistan (3.24), Bosnia-Herzegovina (3.22), Grenada (3.17), Netherlands (2.92), Australia (-1.44), Bolivia (-1.45), Moldova (- 1.71), and Kosovo (-1.86) from the sample. As we show later, the slight difference between early joiners and late joiners is largely driven by a huge cohort of African countries joining in 2018 whose sentiment has been consistently positive throughout our period under observation, notwithstanding the subsequent crises having occurred since.

All Central Asian countries hold positive views towards the BRI with Turkmenistan leading the way. Kazakhstan which – due to its rich raw materials and its geographical position – has long been at the centre of China’s strategic focus in Central Asia also shows a strongly positive sentiment towards the BRI.

Sub-Saharan Africa’s sentiment towards the BRI is rather positive as well, although certain outliers mark the negative end of the spectrum. For instance, Angola’s view towards the BRI is remarkably negative. Initially, the country had marketed its strategy of oil-backed credit lines as the ‘Angola Model’ of economic development. The eventual failure of sustained growth to materialise and the economic downturn due to the pandemic have put Angola in a state of serious debt distress, with 45 percent of its external debt now owed to China.

In the East Asia and the Pacific region, sentiment is more mixed. Australia – whose diplomatic ties with China have deteriorated quite significantly – holds the most negative sentiment towards the BRI, while Laos has traditionally been enthusiastic about the BRI and its promise of investment.

In the Middle East, Gulf countries such as Bahrain and the United Arab Emirates exhibit strongly positive sentiment towards the BRI, while countries around the levant such as Israel, Iran and Iraq seem to oppose the initiative.

European countries in the EU are generally more positive about the BRI than European countries outside the EU. However, even among the former, large differences can be noted. The Netherlands and Portugal are strongly in favour of the BRI, while Ireland is strongly critical of the initiative.

The two North American countries, Canada and the United States, have from the beginning uttered their opposition towards the Initiative. Top-level US politicians view the BRI as a tool to counter US dominance and to create a China-centred network of alliances. Then secretary of state Hillary Clinton famously accused China of ‘new colonialism’ in 20113. Not surprisingly, this is reflected in US media

sentiment towards the BRI. The US and Canada hold both strongly negative views towards the BRI, - 0.78 and -1.31 respectively.

In Latin America, the image of the BRI is much less clearly defined. Countries vary wildly in their views. Brazil and Mexico, the two largest developing economies in the region, hold negative views of the BRI. The rather neutral stance towards the BRI in many other Latin American countries reflects diplomatic uncertainty associated with it. On the one hand, many Latin American countries do not consider Chinese lending alone to be the source of debt distress, given its limited weight in the region. On the

other hand, countries are not eager to engage in an unnecessary confrontation with the US, Latin America’s most important commercial partner.

In South Asia, Pakistan leads on the positive side. The country has long been at the centre of the BRI and the China-Pakistan Economic Corridor (CPEC) marks a strategically important trade road for China. On the other side, India’s sentiment towards the BRI is clearly negative, unsurprisingly as China and India are both strategic competitors in the region. Further, India plays a vital role in the US attempt to contain a rising China.

We also focus on a cross-sectional comparison based on countries average sentiment towards the BRI. However, the image of the BRI is evolving over time not only because the impact of the BRI takes time to materialise but also because of China’s changing strategy in the implementation of the initiative. In this section, we analyse the time-series evolution of the initiative’s image. Specifically, we investigate whether the change in sentiment towards the BRI simply follows the change in the general image of China.

To track the time-series movement of sentiment towards ‘China’ and the ‘Belt and Road Initiative’, we use GDELT summary to search news with two sets of keywords. Specially, we extract news including both ‘China’ and ‘BRI’ in the first group whereas the second group only contains the news including ‘China’ but excluding ‘BRI’. We use an unweighted mean to calculate the average sentiment across countries. The period under observation is 1 January 2017, to 16 November 2022. Looking at the cross-country averages. Sentiment towards the BRI is much more positive than sentiment towards China. This confirms that countries differentiate between the gains of economic cooperation and China as a model in the world.

The selected time range is between 1 January 2017 and 16 November 2022. The spikes in sentiment coincide with the convening of the UN General Assembly where reporting on the BRI is more positive. The difference in the trendline diminished from approximately 1.5 sentiment points at the beginning of 2017 to 1 sentiment point in the final quarter of 2022 indicating that the image towards the BRI deteriorated faster than the image towards China in general. While our analysis is descriptive, we suspect several factors influencing the change in sentiment. First, countries might be subject to a levelling effect reflecting initial enthusiasm towards infrastructure investment that has cooled down over time. Second, debt distress in recipient countries – partially triggered by the pandemic – has sparked criticism towards the initiative in the media. And third, increasingly negative reporting in Europe and North America as a result of China’s investment activities in high-technology sectors triggered a shift in sentiment. To investigate the validity of these three factors, we deploy once again a regional decomposition.

For countries that had no media coverage in 2022, we used values for 2021. At a first glance, the image of the BRI has deteriorated across all geographies, though not by an equal magnitude. In general, sentiment decreased much less in developing countries than in the EU and North America, lending support to our suggestion that sentiment change is driven disproportionately by Western economies. In Central Asia the initiative has deteriorated from an exceptionally high average value of 3.08 to a still strongly positive value of 1.72. This in turn lends credibility to a levelling effect, at least with respect to Central Asia and possibly Europe. The drop in sentiment was much smaller in South Asia, the Middle East and North Africa and sub-Saharan-Africa, although it turned negative for the former two regions. Finally, debt distress in recipient countries which occurred predominantly in sub-Saharan Africa does not seem to have affected sentiment across the board. Note, that among the 34 countries abstaining with China in the UN resolution on the war in Ukraine in February 2023, most were Central Asian and sub-Saharan African, indicating that a positive view of the BRI is at least correlated with political alignment on the global stage.

The EU is the region that has most moved away from a positive sentiment towards the BRI. Indeed, by focussing on the EU’s perception (Figure 10) we can see that – except for the Czech Republic, Cyprus, Latvia and Estonia – all EU countries reported a more negative image of the BRI in 2021/22 than in 2017. This is again not surprising as events have spiralled since then. The EU’s labelling of China as a ‘systemic rival’, tensions about Chinese investment in Europe’s high-tech sectors, negative reporting on BRI projects and the COVID-19 pandemic have cast a shadow over the relationship between the two global players. Whatever combination of factors is behind the almost invariable deterioration of sentiment, the EU has appeared much more cautious now in its diplomatic engagement towards the Middle Kingdom, especially after Western dreams to induce political change in China through economic cooperation have backfired. Instead, the European Commission has promoted its own alternative to the BRI, namely the ‘Global Gateway’ and is in the midst of redefining its relationship with the African continent.

Chinese engagement in sub-Saharan Africa has been a hotly debated topic as of recently. China’s investment in the forgotten continent picked up in 2005 as part of the central government’s ‘China Goes Global’ strategy. Since then, China’s foothold in Africa has been increasing and as of 2020, China represents the main source of African imports in goods. In Figure 10 we disaggregate our sentiment indicator by country focusing on sub-Saharan Africa. As has been confirmed by scholarly work, China’s story in Africa seems far from uniform and has to be evaluated on a case-bycase basis. Several countries that were initially positive about the BRI have changed their view to neutral or even negative. These include Tanzania, Zambia, Zimbabwe, Ethiopia and Kenya. Other countries who were sceptical in the beginning now view the initiative in a favourable light. Those include Rwanda, Cameroon, Malawi and the Seychelles. At the same time, the extreme examples illustrate the complexity of engagement and challenges China faces in Africa. Tanzania, for instance, moved away from BRI engagement after the Chinese side expressed concerns about political volatility and withdrew from planned projects. In Zambia, the country’s debt crisis has been blamed on the failure of BRI projects to deliver the expected large-scale economic benefits it promised. Both countries have shifted their view from strongly positive to neutral. On the positive extreme, Cameroon even moved beyond economic cooperation with China into military collaboration. The Seychelles – having received Chinese funding for important government buildings, including the parliament – recently agreed to deepen cooperation in environmental protection with China8. Both nations favour the BRI now more than in 2017, with a recent sentiment score of 1.71 for Cameroon and 1.36 for the Seychelles, respectively.

Finally, research shows a decomposition of the change in sentiment across China’s neighbourhood, including Central, South and Southeast Asia. Notably, sentiment has decreased across the board except for a few selected countries, some of which had a prominent role in China’s overseas lending. The exceptions include Brunei, Mongolia, the Maldives, and North Korea. Cambodia, Indonesia and South Korea did not shift significantly, and are still quite positive. All other countries, most strongly Vietnam, Singapore, Thailand, and Australia, either went from positive to neutral, or from neutral to negative. The decomposition also reveals that South Asia’s rather negative sentiment is largely driven by India whose sentiment indicator stands at a value of -1.31 in 2022. Southeast Asia on the other hand remains deeply split, even within the ASEAN states. As of today, Brunei, Indonesia and Cambodia still strongly favour the initiative, while the initiative’s image in Myanmar, Thailand, and Singapore has significantly worsened. Countries of strategic importance for the US in its attempt to contain China, namely India, Japan, and Australia are found at the lower end of the sentiment scale

We have analysed the sentiment towards the Belt and Road Initiative in the world using a large open-access dataset, namely GDELT. The key finding is that most regions in the world hold a rather positive view towards China’s BRI, although wide differences appear across regions and countries. North America and South Asia hold a negative view of the initiative, while Central Asia and sub-Saharan Africa display are most positive. We also find that countries not having signed an MoU have a more negative image of the BRI than ‘Early Joiners’ and ‘Late Joiners’. Further, our results show that – although average sentiment is positive – the sentiment towards the BRI has deteriorated.

The analysis suggests that this trend is only partially connected to the deterioration of China’s image in general. In fact, the sentiment towards the BRI has deteriorated faster than the sentiment towards China as a country. We also document that sub-Saharan Africa, where debt restructuring has been most frequent still holds a positive view of the BRI. The regional discrepancies in sentiment and the deterioration of the BRI’s image will have lasting effects on the nature China’s foreign policy engagement. Several key policy implications can be extracted: As a consequence of the BRI’s deteriorating image in Western economies, the Chinese leadership will most likely concentrate its diplomatic efforts on regions that are still positive towards the BRI, namely Central Asia and sub-Saharan Africa. With its current engagement in the UN and its emphasis on South-South cooperation this is already well under way. Due to the strategic importance of these regions for European economies, the EU must step up its efforts in these geographies while keeping in mind the complexities on the ground.

The EU can expect the Chinese government to adjust the narrative behind the Belt and Road Initiative in response to a generally deteriorating sentiment. Initial indications are already observable. Chinese foreign policy elites now frequently speak about ‘Belt and Road Cooperation’ instead of ‘Belt and Road Initiative’ which sounds less like a strategic push towards a nationalist goal9. Besides, several new concepts have appeared that complement the Belt and Road Initiative, notably the ‘Global Development Initiative’ and the ‘Global Security Initiative’. It seems clear that any analysis of the future of the BRI needs to take into account the evolving sentiment as well as China’s reaction to it, which also implies a rapidly changing narrative, as a way to adapt to the growing challenges.

By Alicia García-Herrero and Robin Schindowski on April 25 2023 for Bruegel.