The international financial system is dominated by the US. Washington has often used its clout in the international financial system to further its economic and geopolitical interests through financial sanctions. As antagonism between the US and China moves beyond trade and technology, how the US-China rivalry will play out in the new stage of international finance is a matter of great concern to the world.

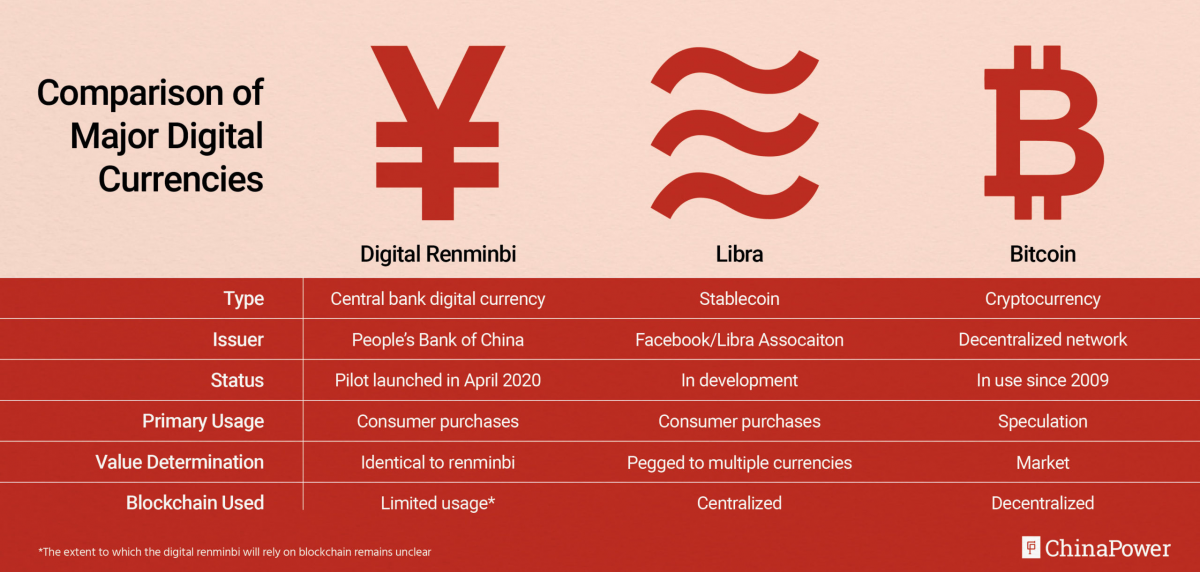

China has been working on a Central Bank Digital Currency (CBDC) since 2014, and is intensifying its efforts to internationalise the Renminbi.

On the surface it appears the CBDC will be for domestic use, but a CBDC will simplify cross border transactions. For a long time, the country has been dissatisfied with the U.S. Dollar’s (USD) ongoing role as the global reserve currency and is committed to extending its currency’s reach.

It even has an initiative to denominate international trade credit in Renminbi (RMB) rather than dollars. And the Belt and Road Initiative has seen China extend more than $1 trillion in foreign loans.

At a recent online global seminar organised by the Pangoal Institution China and the Centre for New Inclusive Asia Malaysia, experts from China, Russia, Europe and the US deliberated and disussed the issue.

One of the key speakers was Mr Ali Amirliravi, CEO and Founder of LGR Crypto Bank of Switzerland. and creator of the Silk Road Coin digital currency.

He addressed China’s vulnerability to the global financial system, and said:

“This is a very interesting question as there are a lot of factors to consider. To begin, I think it might be helpful to define China’s vulnerabilities specifically. We are speaking about international finance here (it’s a very complex and politically charged system) and since the second world war, the space has been more or less dominated by the interests of the US. We see this in the global dominance that the US dollar has held for the last 70 years. We see that in the steps that Washington has taken to ensure that the dollar acts as the global reserve currency - particularly in industries like the global oil trade. Up until quite recently, it was probably difficult to even imagine a global financial system that was not directly supported by the US dollar.

By virtue of this global reliance, the American political machine was given significant power to wield in international finance. The best evidence of this can probably be found in the history of crippling economic sanctions that the US has enacted against specific states - the impacts of which can be devastating. In a nutshell, it’s an asymmetrical power dynamic wherein the US has carved out a significant negotiating advantage over other countries.

Put it this way: when the global economic system is built to fit the domestic currency of a specific state, it is easy to see how that state would be able to tailor certain policies and promote behaviours that would further their own geopolitical interests - this has been the American reality for the last few decades.

But things change. Technology advances, political relationships evolve, and international trade and money flows continue to expand and grow - now incorporating more people, countries and businesses than ever before. All of these factors (economic, political, technological, societal) work to shape the reality of the international order, and we are now at a place where a serious discussion about a replacement for the US dollar is warranted - that’s why I am excited to be here speaking about this issue today, it’s really time to have the conversation.

So, now that we have set the scene, let’s tackle the question: could the creation of a digital Renminbi address the vulnerability and asymmetry that China is dealing with in international finance? I really don’t think this is a simple yes or no answer here, in fact I think it is valuable to consider the question with a broad outlook on development over the next few years.

Starting with the short term, let’s put the question like this: will the digital renminbi have significant impact internationally immediately following launch. The answer here I think is no, and there are a few reasons for that. First of all, let’s consider the intention of the issuer, the Chinese central bank. Reports show that the initial focus of the DRMB project is domestic, the Chinese government is looking to challenge private sector digital payment methods like AliPay etc., and getting the broader population used to the idea of Central Bank-issued digital currencies powering the majority of economic transactions in the country. To put it simply, the scope of the first stage of the DRMB launch is too small and domestically focused to directly impact the international system - there just won’t be enough DRMB in circulation globally.

There is another point to consider in the short-term: voluntary acceptance. Even if stage one of the DRMB project did have an international focus and was committed to minting huge amounts of digital currency, international impact requires international use - meaning that other countries would have to voluntarily accept and support the project in the early stages. How likely is this to happen? Well it’s a bit of a mixed bag, we’ve seen a few agreements start to pop-up between China and some countries in Central Asia as well as South Korea and Russia, which outline future frameworks for DRMB acceptance and trade, however there isn’t too much in place yet. And that’s just it: before the DRMB can have international impact, there needs to be widespread international access and acceptance, and I don’t see that happening in the short-term.

Let’s move to a mid-term analysis. So imagine that phase 1 of the DRMB is complete and we have individuals and corporations in China accepting, transacting and trading it. What will phase 2 look like? I think we will start to see China expanding the scope of the DRMB project and incorporating it into their international development and infrastructure projects. If we consider the scope of the Belt and Road Initiative and China’s commitments and focus on development and investment across central Asia, Europe and parts of Africa, it is clear that there are many opportunities to promote and incentivize use of the DRMB internationally.

A great example to consider is the group of countries that make up the Silk Road area (about 70 countries). China is participating in infrastructure projects here, but it is also promoting increased trade in the area - and that means a lot of money moving cross-border. This is actually an area that my company LGR Crypto Bank is focused on - our goal is to make cross-border payments and trade finance transparent, fast and secure - and in an area with over 70 different currencies and incredibly disparate compliance requirements, this is not always an easy task.

Here is precisely where I think the DRMB could add a lot of value - in clearing up the confusion and opacity that comes with cross-border money movement and complex trade finance transactions. I believe that one way the DRMB will be marketed to China’s trade and development partners is a way to bring transparency and speed in complicated transactions and international transfers. These are real problems, especially in the multi-commodity trade business, and they can cause serious delays and business interruptions- If the Chinese government can prove that adoption of the DRMB will address these issues, then I think we will see real eagerness in the market.

At LGR Crypto Bank, we are already researching, modelling and designing our own money movement and trade finance platforms to work in harmony with digital currencies, particularly our own Silk Road Coin and the Digital Renminbi - we are ready to offer customers the best in class finance options as soon as they are made available.

When it comes to the international stage, I think that China will use its BRI as a proving ground for the DRMB in real-world commerce. By doing this, they will start to develop a network of DRMB acceptance across the Silk Road Countries and will be able to point to successful infrastructure projects as proof of the success of the Digital Renminbi. If this phase is carried out properly, I think it will create a very good foundation of DRMB acceptance that can be built on and expanded globally. The next step would likely be Europe - this is something of a natural extension of the Silk Road Area, and also ties in to the reality of increased trade between the EU and China. It’s important to note that if we consider all of the domestic economies that make up the Euro block together, it is the largest importer/exporter in the world- it would be an incredible opportunity for China to bring international attention to the DRMB and prove its capabilities in the West.

In the long-term, I do think that it is possible for the DRMB to gain high levels of international traction and achieve some level of global acceptance. Again, it will all depend on the success of the Chinese government in making the case for adoption throughout the earlier phases. The value propositions of central bank digital currencies are very clear (increased transaction speed, improved transparency, fewer middlemen, less delays, etc.), and China is certainly not the only one developing such an asset. Currently, however, China is a leader and if they can execute an expansion plan without too many issues along the way, this head-start could make it difficult for other state offerings to catch-up. Maybe not, though.

It could be that in the long-term, all states will have a sovereign digital currency - and this begs the question: in the age of digital currencies, is there still a need for a global reserve currency? I’m not sure. What would the value add be of a reserve currency when central bank digital currencies could be traded effortlessly with immediate settlement times? Maybe reserve currencies will simply become a relic of an outdated financial system.

Looking forward to the long-term, I can imagine 2 scenarios where the DRMB could alleviate China’s vulnerabilities in the international financial system:

The DRMB becomes the new world reserve currency

The notion of a world reserve currency becomes obsolete and the new economic order runs on state-backed digital currencies operating without a hierarchy.

Whatever happens, I do believe we are on the cusp of a major change in global finance. There is no doubt that digital currencies, specifically central bank digital currencies, will play a massive role in defining the new economic paradigm. I believe that China is making great moves in leading the pack on this, and I know that at LGR Crypto Bank we look forward to adopting the DRMB where we can to further optimize and expedite the money movement and trade finance solutions that we offer to our customers.

By Colin Stevens on October 14 2020 for the EU Reporter.